Be duitful

with your duit.

Track your money, debts, loans, and savings. Kill high-APR debt with the avalanche method, and keep every cent on your phone. Encrypted on-device. No account, no subscription.

On Android? Join the beta track →

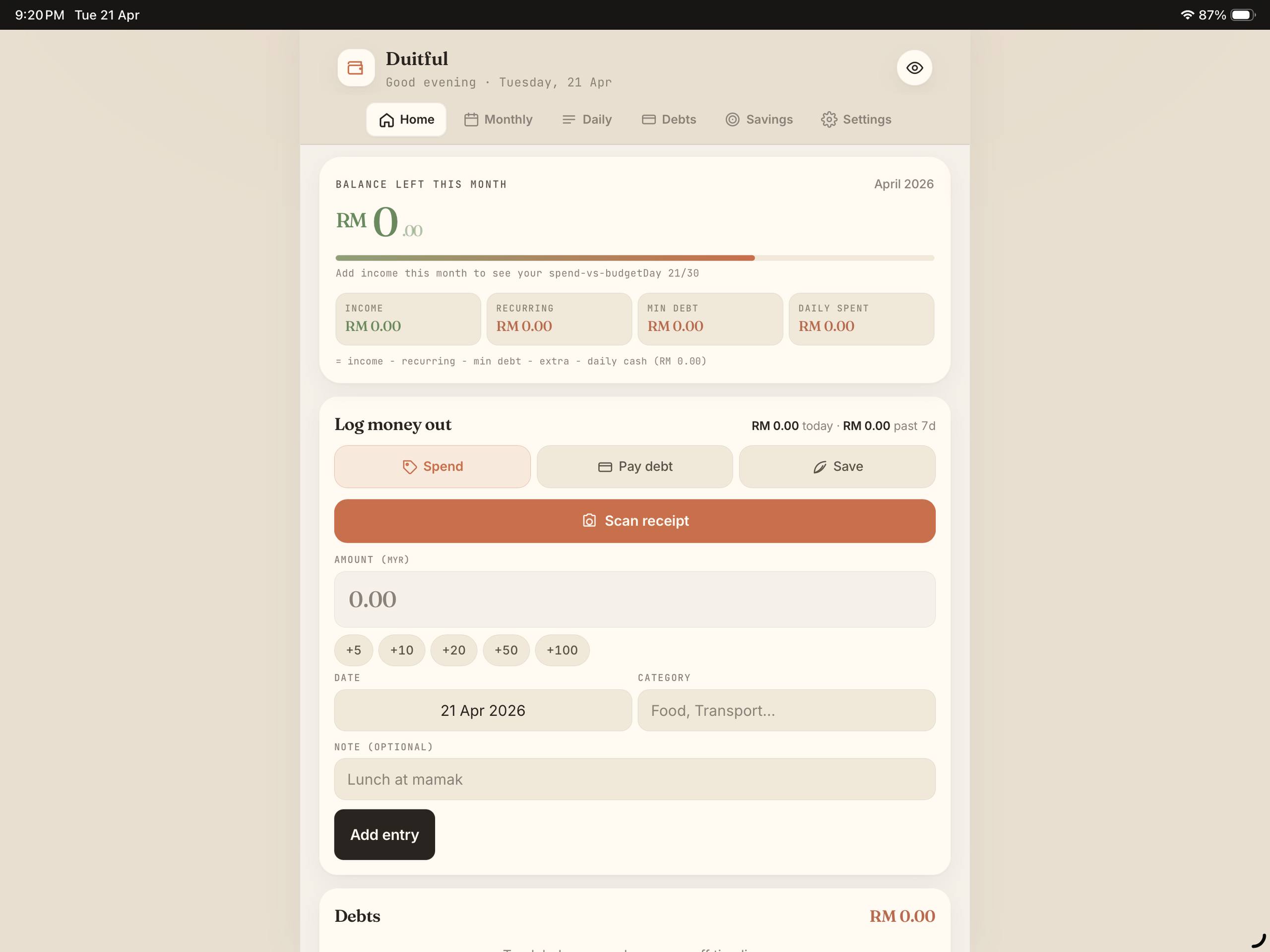

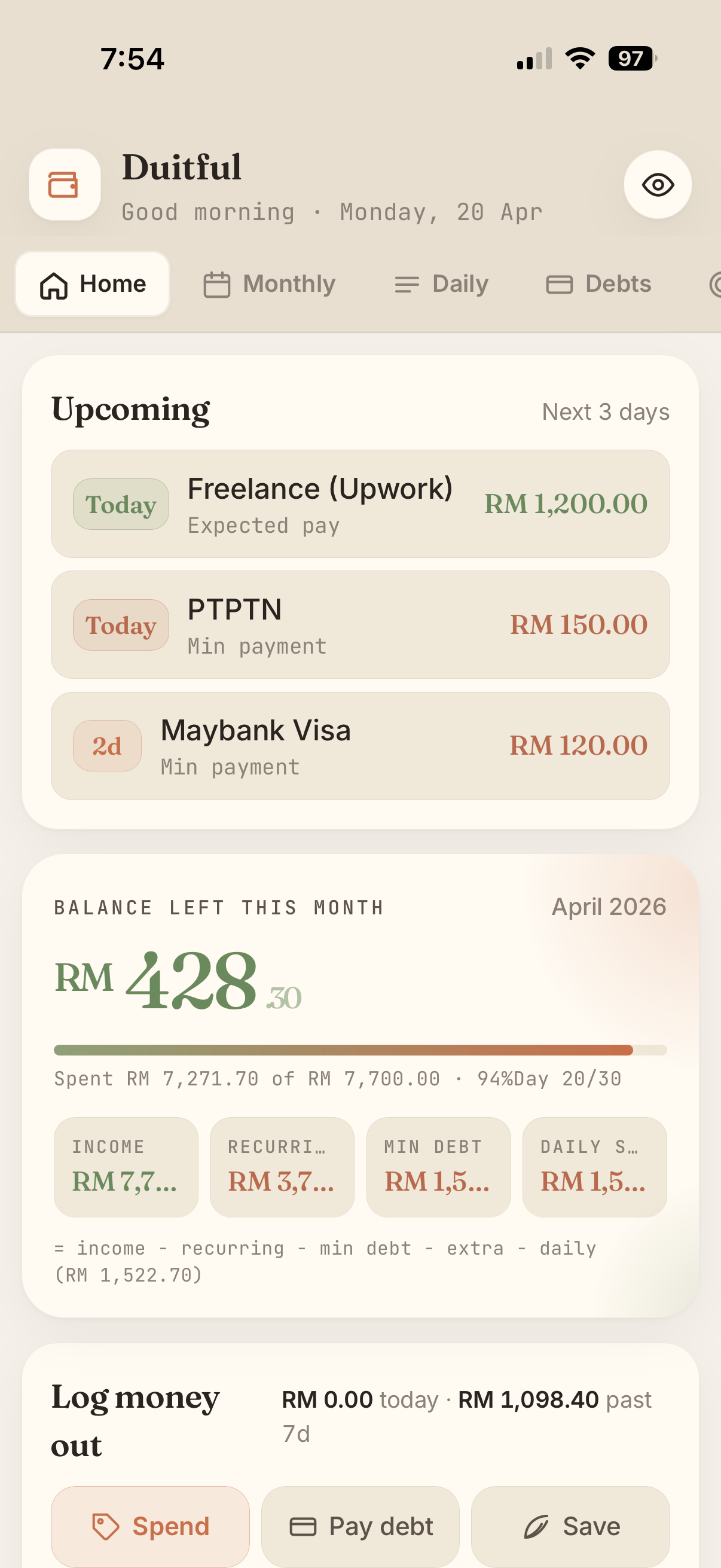

Track what's actually

leaving your account.

Most trackers ignore the bits that hurt most: high-APR cards, BNPL instalments, foreign-currency subscriptions. Duitful was built around all three.

Debt avalanche

Prioritises your highest-APR debts first so you pay less interest overall. Watch your exact debt-free date shift with every payment.

Payoff timelineBNPL & installments

Track Atome, SPayLater, Grab PayLater and card installments in one place. No more surprises from that phone you bought six months ago.

SEA-nativeReceipt OCR + auto-FX

Snap a receipt and Duitful pulls the amount, merchant, and category. Foreign currency converts to MYR automatically at the day's rate.

3 scans/mo freeOn-device encryption

Every entry is AES-GCM encrypted with a passcode-derived key. Nothing leaves your phone — not even Duitful can read your data.

AES-GCM · PBKDF2Pay once, keep it

RM 19.90 lifetime Pro. The free tier is permanent. No trial, no subscription, no expiry emails.

Lifetime · no subsiPhone, Android, iPad, desktop.

Same app, same data. Install to home screen on any OS — no app store needed. Pro syncs every device through your own Google Drive (encrypted with your passcode before it leaves the phone).

Your money data

never leaves your phone.

Most trackers send your transactions to a server, then charge you a subscription on top. Duitful keeps your data on your phone, full stop. Encrypted, passcode-locked, no sync server to breach.

-

EncryptionAES-GCM at rest, PBKDF2 key derivation

-

AccountsNone. No email. No sign-up.

-

AnalyticsNone on your data. None ever.

Pay once. Keep the app.

The free tier is permanent. Pro is a one-time purchase, because a tracker for your money shouldn't cost more than the money it helps you save.

- Up to 3 debts

- Up to 2 savings goals

- 3 receipt scans per month

- Manual expense & income tracking

- Full on-device encryption

- Unlimited debts, goals and receipt scans

- Multi-currency entry in 40+ currencies at daily rates

- Budget pools with rollover and per-month overrides

- Auto-recurring monthly income and bills

- Android auto-capture and encrypted Drive sync

- Every future Pro feature, included see changelog

Built by one person, in Malaysia, for Malaysians.

I'm Aydil. Duitful started as an Excel sheet I built for a friend struggling with cash flow. The paid apps I'd tried either pushed a monthly subscription forever, kept asking to link my bank, or sold my data on the side.

Duitful is the tracker I wanted: pay once, own it forever, built for ringgit from the ground up, and your data never leaves your device. If it's missing something Malaysia-specific, that goes to the top of the roadmap — drop a note at [email protected].

Honest disclosure: most of the code and a lot of this page were written with Claude Code. The product idea and what ships are mine — full source on GitHub.

— Aydil, Kuala Lumpur

The short answers.

Why one-time pricing and not a subscription?

A money tracker shouldn't cost more than the money it tracks. Pro is RM 19.90 once. You keep the app, get every future Pro feature, and never see a renewal email. Server costs are near-zero because your data stays on your phone — a subscription would just fund our growth chart.

Does my data really never leave the phone?

Correct. All your transactions, debts, and goals live in an AES-GCM-encrypted database on your device, locked with a PBKDF2-derived key from your passcode. There is no sign-up, no sync server, no analytics SDK on your financial data. Receipt OCR happens via a privacy-focused API only when you explicitly scan, and no receipts are stored remotely.

Which banks are supported for auto-capture?

On Android, Duitful parses notifications from major Malaysian banks and e-wallets: Maybank, CIMB, Public Bank, RHB, Hong Leong, HSBC, TNG eWallet, GrabPay, Boost, Shopee Pay, and more. You review each transaction before it's saved. iOS doesn't allow notification reading, so on iPhone you'll use receipt scans and manual entry instead.

What happens if I lose my passcode?

Your data cannot be recovered — that's the trade-off for real end-to-end privacy. Duitful never has a copy of your passcode or data, so it can't reset for you. Write your passcode down somewhere safe, or use Pro's encrypted backup to restore to a new device.

How does Pro sync across devices?

Through your own Google Drive — not a Duitful server. Your encrypted database lands in a hidden app folder. Other devices sign in with the same Google account, pull the file, and decrypt it locally with your passcode. The passcode never leaves your device, so the data in Drive is unreadable to Google and to me.

How-tos for Malaysian money.

Petrol subsidies, tax relief, freelancer cashflow. The bits no one explains in plain words.

Selangkah Hab Sehat + the financial-stress loop

Free screenings on Selangkah cover the mental-health side; a five-minute Duitful tag covers the money side. Together they make the feedback loop visible.

Scope 3 supplier pressure under NSRF

A practical SME-supplier survival guide for the moment your Group 1 customer asks for emissions data. What to track, what to refuse, and the baseline that holds up.

Malaysia's pivot to AI-native banking

The Ministry of Digital wants AI inside the core, not bolted on. What changes for the apps you use, the loans you apply for, and the budgets the AI watches for you.

Ready to be duitful?

Start on the web today. The Android app is in open beta — beta testers wanted. iOS coming soon.

On Android? Join the beta track →